Gold price supported by central banks that continue to actively buy

Since the January peak, gold has had a visibly harder time. That weaker price movements At first glance, it may seem like a sign that the market is losing momentum, but below the surface, an important pillar simply remains intact: central banks are still buying net gold.

And that is fundamentally relevant. Because in recent years, central banks have been one of the most important structural sources of demand for gold.

Gold cools after a strong start to the year

After the January summit, the gold price start moving less convincingly. This is in line with a market that is temporarily catching its breath after a strong advance. Moreover, we see that central banks, like other buyers, are not completely blind to the price. If gold rises sharply, the pace of purchases may slow down somewhat.

However, weaker price movements do not automatically mean that fundamental support has disappeared under gold. On the contrary: the numerals about February, on the other hand, show that central banks have become clearly more active again after a quiet month of January.

In addition, we should not exaggerate the weakness of gold. After the extreme increases of the past year, a short breather is not immediately disastrous. Even if we take the performance of the past three months, gold still has a positive return of 3.83 percent.

In addition, the 200-day price average (blue) and the 200-day exponential price average (red) strongly supported the gold price in March.

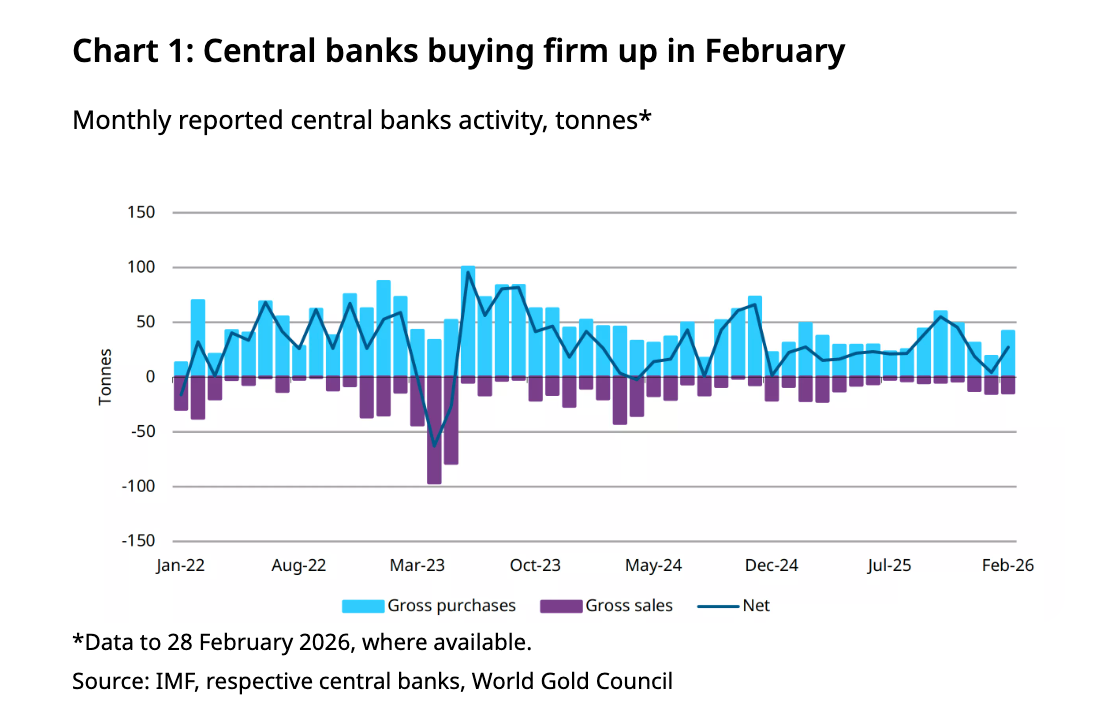

Central banks bought 27 tonnes of gold net in February

According to World Gold Council figures, central banks bought 27 tonnes of gold net in February. As a result, February was clearly stronger than January, when activity temporarily declined. The February level is also in line with the average monthly pace of 2025.

Over the first two months of 2026, the net purchase thus amounts to 31 tons. That is lower than in the same period last year, when central banks had already added 50 tons together, but it confirms that gold continues to play a strategic role in reserve policy.

Poland stands out as the largest buyer

The main buyer in February was the Polish central bank, which added 20 tons to reserves. In doing so, Poland brought its total gold supply to 570 tons, accounting for around 31 percent of the total reserves.

That is significant. Poland has been one of the most consistent buyers on the gold market for some time and is once again showing that it sees gold as a structural part of its financial buffer. The fact that the Polish central bank has even set a target of 700 tons of gold shows how serious that policy is.

China, Uzbekistan and other central banks also continue

In addition to Poland, other well-known buyers also remained active. Uzbekistan added 8 tons and is now on five consecutive months of purchases. Kazakhstan also purchased 8 tons. The Czech Republic, Malaysia, China and Cambodia also added gold.

The ongoing purchase series are particularly striking. The Czech Republic is now on 36 consecutive months of purchases. China has now bought gold for sixteen months in a row. Such series are important because they show that gold is not a quick trade for these central banks, but a strategic choice.

Sellers don't change the bigger picture

In February, there were also some sellers opposite buyers. Turkey saw the biggest drop of 8 tons, followed by Russia with 6 tons. In the case of Turkey, according to the text, this seems to mainly have to do with liquidity management and foreign exchange transactions.

It is important that this does not automatically mean that gold will fall out of favor as a reserve asset. Especially in the case of Turkey, it seems to be rather a temporary use of gold for financing and swapping purposes. The Turkish central bank itself also indicated that a significant part of these transactions can later flow back to reserves.

Africa and emerging markets show new interest

A second important development is that more and more central banks in emerging markets are looking to gold as a strategic diversification tool. Uganda and Kenya are examples of countries where there is an interest in investing in gold increases.

This is fundamentally positive for the long term. The wider the group of official buyers becomes, the stronger the structural demand base for gold. Especially in a world where many countries want to be less dependent on traditional reserve currencies and have become more sensitive to risks in the international financial system, gold remains a logical choice.

So the message is: the weak price movement since January deserves attention, but it does not mean everything. In the short term, gold can best correct or consolidate, especially after a strong rise. But on a fundamental level, one of the most important sources of demand simply remains present.

The fact that central banks were clearly net copper again in February shows that gold still plays a strategic role for official institutions.

Conclusion

Central banks continue to buy gold, laying a firm floor below the price, despite the recent cooling. With strong and sustained demand, gold remains an attractive and strategic long-term investment.

Thom Derks writes for GoldRepublic on gold, macro-economics and geopolitics. He studied Law in Leiden and Economics in Amsterdam. His personal fascination with scarcity and store of value through both bitcoin and gold brought him into the world of financial journalism. Through his own newsletter De Geldpers on Substack, he reaches over 5,800 subscribers with analyses on markets, geopolitics and the monetary system.