Central banks buy large amounts of gold and push the price higher

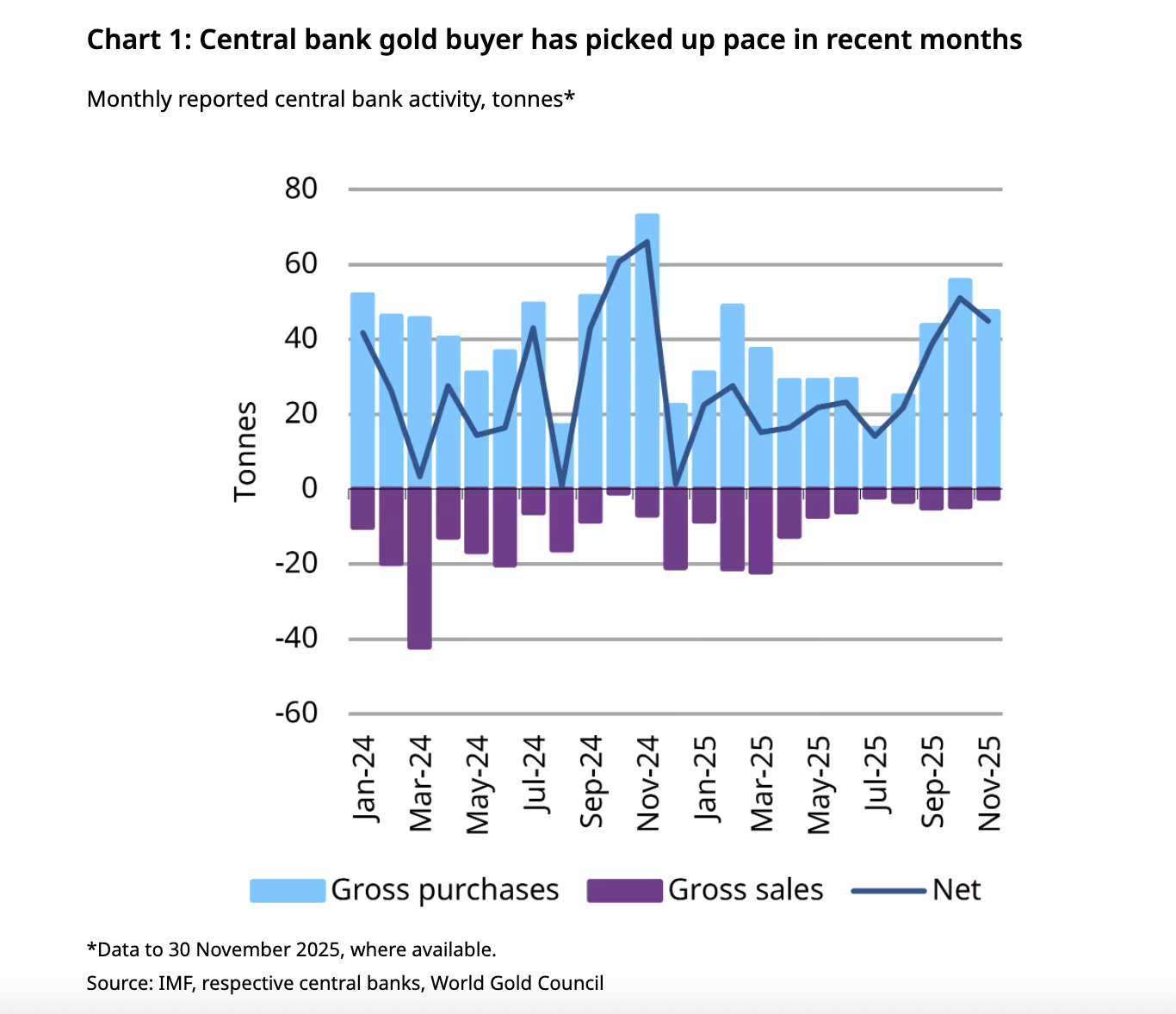

The gold price went off like a charm in 2025, and will continue to rise sharply in the new year for now. This is partly the result of the buying spree of central banks, which conform new figures also add a considerable amount of gold to their reserves in November.

According to the World Gold Council, central banks around the world added 45 tons of gold to their reserves. This means that the pace is slightly slower than in October, but demand remains clearly higher than during the first months of 2025, and in that regard, central banks also appear to be sensitive to the hype around precious metals.

Historic amount of gold purchased by central banks

For the first 11 months of 2025, the reported gold purchase from central banks amounts to 297 tons. This is less than in the record years of 2022 and 2023, but it is still historically high. It is also interesting that most of the purchases come from central banks outside the West.

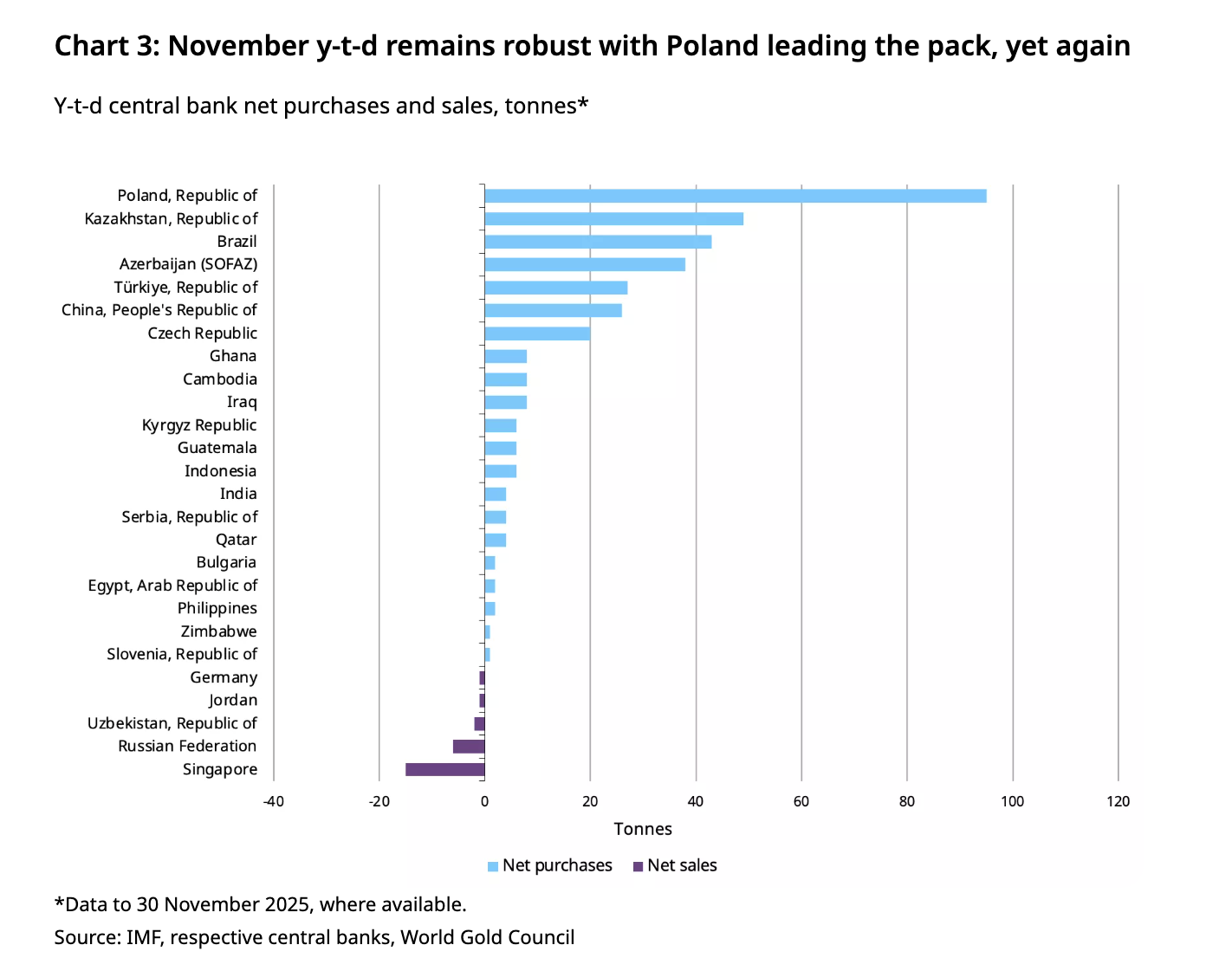

The National Bank of Poland was again the largest buyer in November, buying 12 tons of gold. This brings Poland's gold reserves to 543 tons, accounting for almost 28 percent of the country's total international reserves. Poland is by far the largest buyer this year, with a total of 95 tons.

Other countries were also active. Brazil's central bank bought gold for the third month in a row and added 11 tons in November. Over the past three months, Brazil has purchased a total of 43 tons of gold. In addition, countries such as Uzbekistan, Kazakhstan, Kyrgyzstan, the Czech Republic, China and Indonesia also further expanded their gold reserves.

On the sales side, it remained limited: only Jordan and Qatar sold small amounts of gold.

Non-Western focus on gold

What is particularly striking is that the urge to buy comes almost entirely from non-Western countries and emerging economies. That is no coincidence. Since Russia's invasion of Ukraine in 2022, gold's role within national reserves has fundamentally changed, or rather revived.

After the start of the war, hundreds of billions of dollars in Russian currency reserves were frozen by Western countries. Most of these reserves were in dollars and euros and were located within the Western financial system. For many countries, this was a wake-up call: owning foreign currencies does not automatically mean full control over that capital.

If you look at the chart, you see 2022 almost as a tipping point for the US dollar. Countries and investors alike seem to have realized since then that the new geopolitical reality requires a different approach. A wider and healthier spread simply offers more protection for the future.

In concrete terms, this means: less dependence on the dollar, more room for other international currencies and a greater role for gold as a strategic anchor.

Gold as a protection against geopolitical risk

Since then, many countries have realized that reserves should not only be liquid, but also politically neutral. Gold fits that profile exactly. It is a physical asset, has no counterparty and cannot be frozen by a foreign government or central bank.

For countries that have less geopolitical influence, or that are aware of their vulnerable position within the international financial system, gold has thus become more attractive than government bonds or bank deposits in dollars or euros.

This also explains why countries such as China, Brazil and several Central Asian states continue to structurally increase their gold reserves, despite higher gold prices.

Trust in the dollar system under pressure

Although the dollar is still the world reserve currency, the freezing of Russian assets has visibly affected confidence in that system. Not so much with allies of the United States, but rather with countries that see their geopolitical position as uncertain.

The case for these countries is increasingly: diversification is no longer a return issue, but a strategic necessity.

Although the pace of gold buying this year is slower than in the peak years, the underlying trend remains intact. As long as geopolitical tensions remain high and confidence in the neutrality of the international financial system is under pressure, it is logical that non-Western central banks in particular will continue to see gold as a safe haven.

What is the impact of central banks' buying spree on gold prices?

It is tempting to draw a direct line between central banks' gold purchases and the rise in the price of gold, but it is not that simple. The gold market is large, global and driven by multiple factors at the same time, such as interest rate expectations, the dollar, inflation, and investor sentiment.

Nevertheless, we can roughly outline the order of magnitude.

In November, central banks purchased around 45 tons of gold, while annual gold production in 2022 was around 3,500 tons. With those 45 tons, central banks bought around 15 percent of the total monthly output in November 2025, provided that production reaches the same level for that year.

This is considerable, but probably not such that the price increases in gold are entirely due to the buying behavior of central banks. It remains a significant percentage, but the actual impact of central banks' actions is likely elsewhere.

By adding gold to reserves, these central banks are signaling to the market that they consider the precious metal to be an important asset. This gives investors a bit of confidence: if central banks have their reasons for buying gold, it probably wouldn't look out of place in my portfolio either.

However, we should not underestimate the direct impact of central bank purchases either. After all, they are structural, and generally these entities do not buy to sell the gold again next week or next month. And with all the geopolitical turmoil, it's not unlikely that more and more central banks are replenishing their gold reserves just in case.

Conclusion

Central banks continue to stock up on gold en masse, thereby pushing the gold price further higher. New figures show that the urge to buy will remain as strong as ever towards the new year.

Thom Derks writes for GoldRepublic on gold, macro-economics and geopolitics. He studied Law in Leiden and Economics in Amsterdam. His personal fascination with scarcity and store of value through both bitcoin and gold brought him into the world of financial journalism. Through his own newsletter De Geldpers on Substack, he reaches over 5,800 subscribers with analyses on markets, geopolitics and the monetary system.