Market Update

Dear reader, welcome to the latest GoldRepublic newsletter! In just five minutes, we will fully inform you of current precious metal prices and the most relevant news that affects your investment in precious metals. Don't miss out on these valuable insights!

Stocks at records despite geopolitical turmoil

For investors, the year 2026 is full of contradictions. Whilst the war with Iran is expected to trigger ‘the biggest energy crisis in history’, US stock market indices are hitting one record after another.

Geopolitical turmoil is rife, populism and polarisation are on the rise, yet optimism still prevails in the financial markets. The main reason for this is the enormous promise of the AI revolution, which for the time being outweighs the political and economic uncertainty.

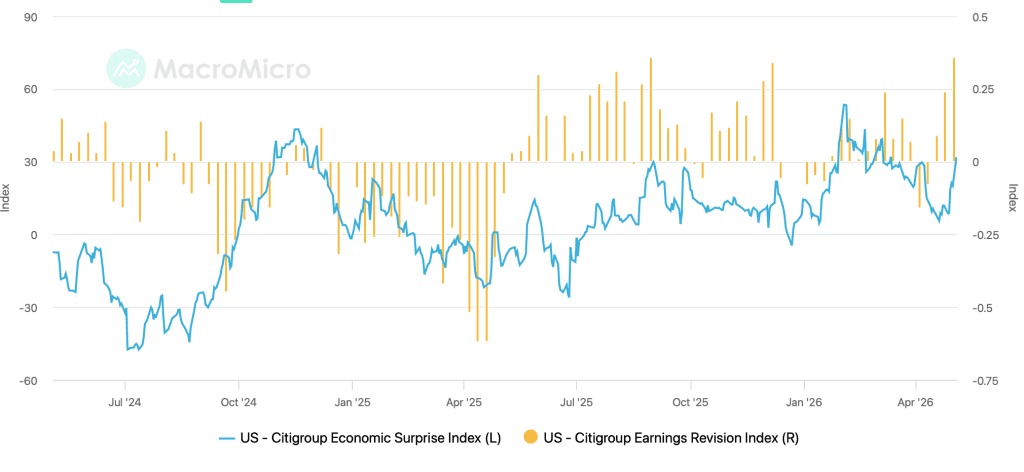

For the time being, the hard data is proving the market right. Economic figures continue to be better than expected, and corporate quarterly results are also remarkably strong. Within the S&P 500, US listed companies are more profitable than ever. Moreover, 85 per cent of companies reported higher-than-expected profits, whilst 77 per cent also saw revenue exceed expectations.

This positive picture received further support again this week. Factory orders in the United States were better than expected, extending the run of positive economic surprises.

This creates a climate in which stock markets can rise, despite the fact that the threat of war with Iran still hangs over the market.

Gold in a Shifting World Order

Although the price of gold has been going through a difficult phase since its January highs, the fundamentals remain promising.

Geopolitical uncertainty remains high. At the same time, the shift towards a new world order is continuing. From a unipolar world, in which the United States was the dominant power for a long time, to a multipolar world in which China and other major powers are also claiming an increasingly significant role.

Furthermore, it remains highly uncertain what the AI revolution will ultimately mean for the global economy. No one can predict with any great certainty which country will be the dominant economic power on Earth in two or three decades’ time.This makes investing in specific shares or economies more difficult, as the winners are less clear. It is precisely this uncertainty that argues for a greater role for assets that are less dependent on economic and political power dynamics.

Put simply: for gold, it makes little difference whether China or America becomes tomorrow’s world leader. For companies such as Apple and Tesla, however, that question is of great importance. The unpredictability of the future paints a favourable picture for gold in the coming years.

After all, it is less certain that an investment in the S&P 500 will pay off as it did over the past decade. That does not mean that investors should immediately shift their entire capital into gold and other independent assets, but it does strengthen the case for doing so.

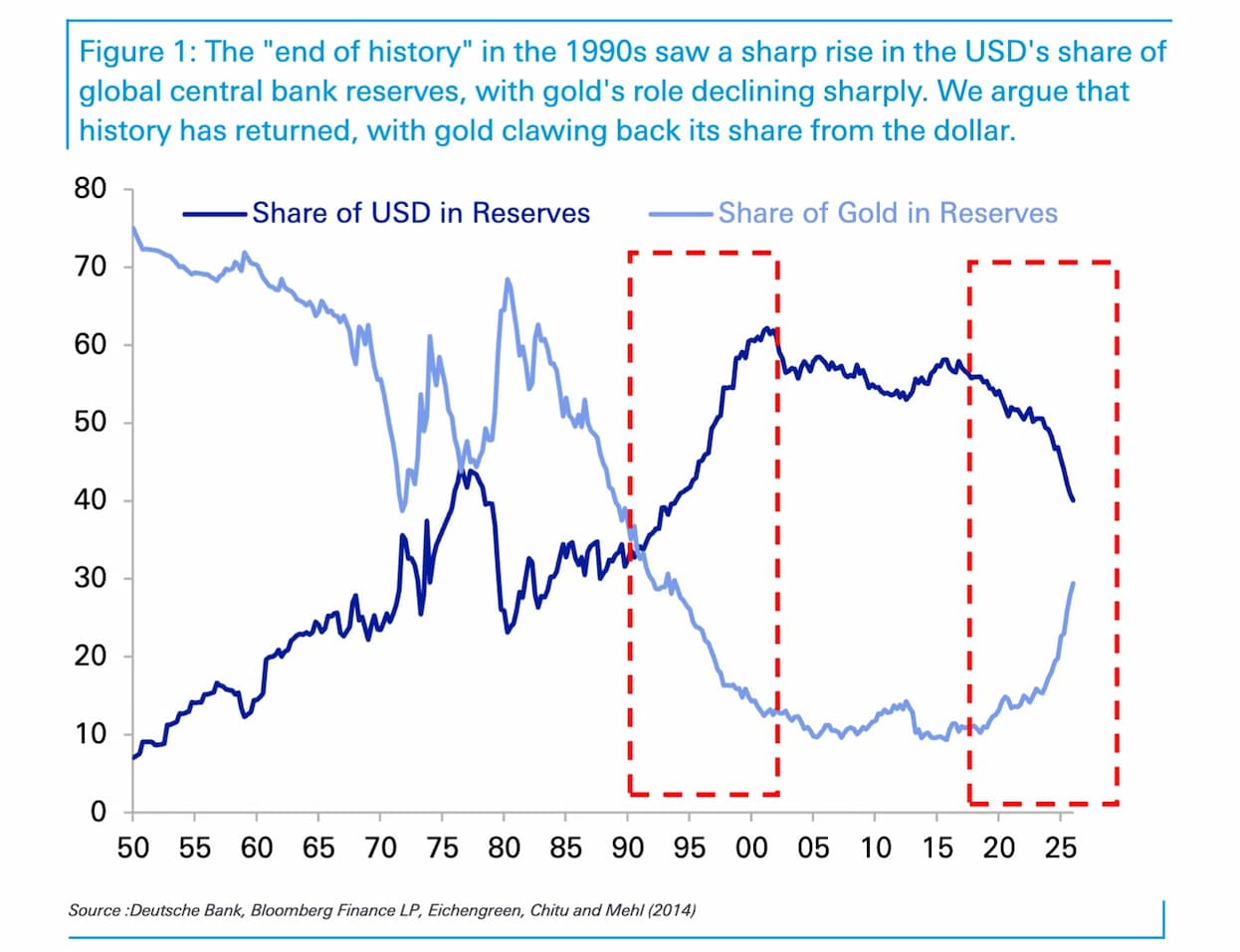

Deutsche Bank recently reached a similar conclusion. According to the banking giant, gold could become one of the biggest winners in a world where countries want to be less dependent on the US dollar.

Central banks in emerging economies, in particular, continue to expand their gold reserves, as gold is not a liability of any government, central bank or company.

In a scenario where gold’s share of global central bank reserves rises from around 30 to 40 per cent, Deutsche Bank even sees scope for a gold price of $8,000 per troy ounce within five years. That is not a firm price forecast, but it does illustrate how significant the structural demand for gold could become if the trend towards de-dollarisation continues.

Momentum now lies with tech, but fundamentals remain strong

As a result, gold is becoming an increasingly suitable addition to a portfolio that takes into account a more uncertain global order. Not as a substitute for shares or productive businesses, but as a counterbalance during a period in which geopolitics, monetary policy and shifts in technological power are harder to predict.

However, a favourable fundamental climate is no guarantee of immediate price rises. Certainly in the short term, financial markets are not just about the story, but also about momentum. Until the end of January, that momentum clearly lay with gold and silver, whilst the US tech market was struggling.

That picture has now reversed. Gold and silver are primarily seeking a bottom and may be laying the groundwork for a new phase of rises, whilst US tech indices continue to break record after record. As a result, the momentum is not currently with precious metals, which reduces the likelihood of a sudden, explosive rise in the short term.

Such phases often begin step by step and only end later in a mass sprint, as we saw in January. The fundamental picture for gold and silver remains strong enough to make such a new sprint possible in the long term, but for now, investors must take into account a market in which attention is once again turning to technology and AI.

Macroscopic: William White

William White, former Chief Economist at the BIS, returns for a candid conversation on the breaking points of the global monetary system.

We discuss the regime change underway at the Fed, why financial repression is already here, the biggest energy shock the world has ever known, and the transatlantic battle over stablecoins versus the digital euro. Bill explains why "banks create money out of nothing," whether AI is the next great malinvestment, what the Mar-a-Lago Plan means for the dollar, and why he believes the endgame ends "not with a bang but a whimper."

Stock markets break records while geopolitical tensions rise. Discover why Deutsche Bank sees gold as one of the biggest winners of de-dollarisation and what this means for your portfolio.

Thom Derks writes for GoldRepublic on gold, macro-economics and geopolitics. He studied Law in Leiden and Economics in Amsterdam. His personal fascination with scarcity and store of value through both bitcoin and gold brought him into the world of financial journalism. Through his own newsletter De Geldpers on Substack, he reaches over 5,800 subscribers with analyses on markets, geopolitics and the monetary system.