.jpg)

Gold temporarily loses ground in the commodity race

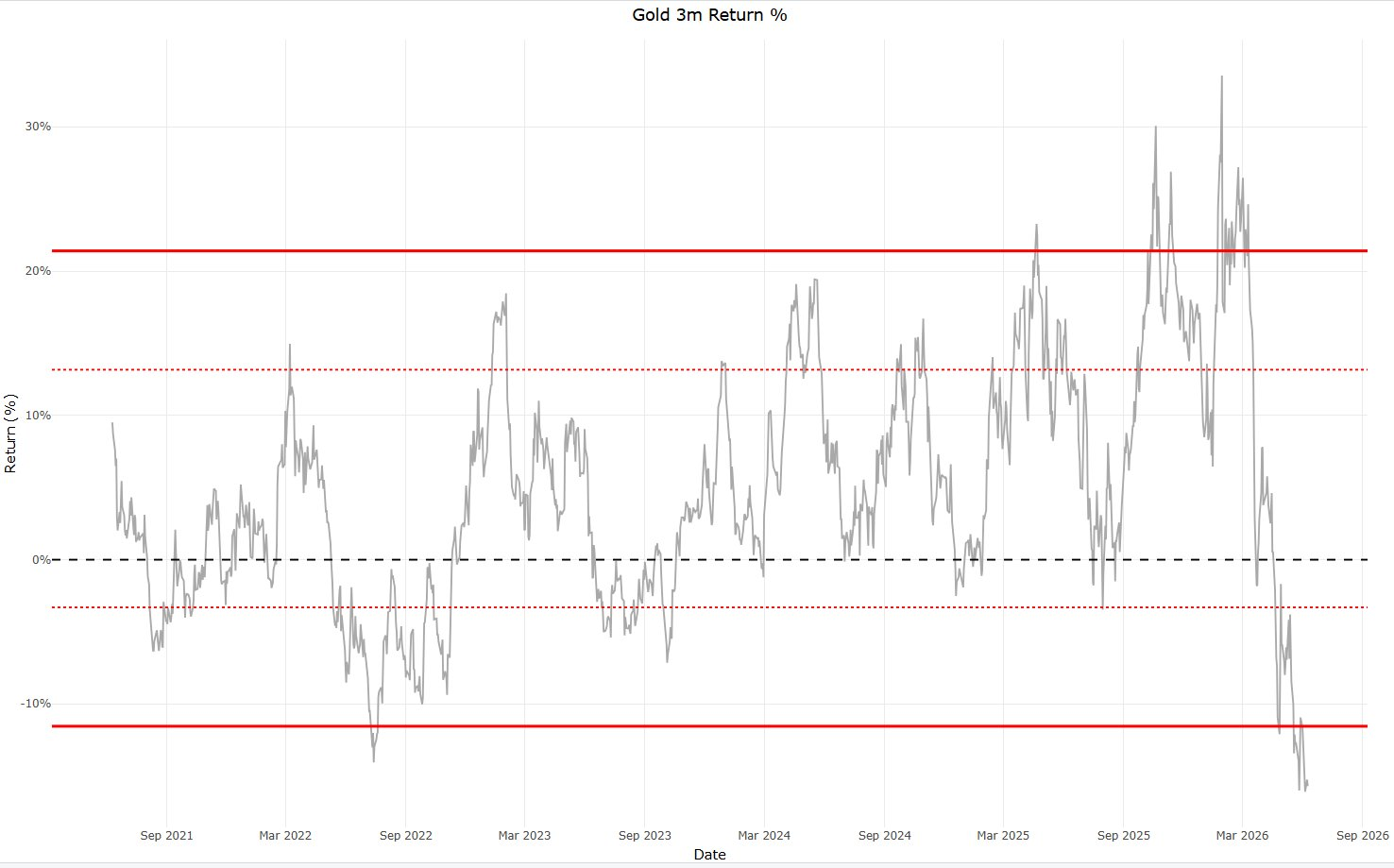

Since the gold price peaked at nearly $5,600 per ounce in January, the precious metal has entered a weaker phase. The past three months were, in terms of returns, even the worst in the last five years. For such price action, there is rarely one clear cause. This time too, multiple developments are playing out simultaneously.

First of all, gold came off an exceptionally strong period. The rally towards January ended in a phase that bore a strong resemblance to a gold rush. The final leg of the rally was driven not only by fundamental demand, but also by momentum, enthusiasm, and the fear of missing out.

The harder an asset rises in the final phase of such a move, the greater the chance of a sharp correction afterwards.

The war with Iran also didn't help in the way you might normally expect. Geopolitical unrest is often favorable for gold, but in this case the war primarily stoked inflation concerns. As a result, bond yields rose and the US dollar gained ground.

That is usually not an ideal combination for gold. The precious metal yields no interest, meaning rising rates worsen gold's competitive position.

On top of that, market momentum shifted after the February decline towards AI stocks. Investors currently appear to be buying almost anything related to artificial intelligence. That capital has to come from somewhere.

In such an environment, gold temporarily fades into the background, along with other assets bought primarily as protection against monetary debasement and systemic risks.

Commodity scarcity pushing gold to the sidelines?

An interesting additional explanation is that a broader commodity scarcity is at play. Due to wars, geopolitical fragmentation, and the massive wave of investment in AI infrastructure, demand for physical commodities is increasing.

Think of energy, copper, silver, uranium, and other materials needed for data centers, power grids, chips, and defense.

In such a world, dollars flow more readily towards commodities directly needed for production and infrastructure than towards gold as monetary insurance. You could say that gold is temporarily competing with the physical building blocks of the new economy.

This makes gold something of a luxury at the moment. Not because the fundamental story has disappeared, but because the market first needs capital for tangible scarcity. Energy, metals, and infrastructure take priority.

Gold only comes back into focus afterwards, once investors start thinking again about the sustainability of debts, deficits, and monetary debasement.

Technical support and fundamental strength remain for gold

Yet that does not mean the technical picture has fully deteriorated. Around the $4,000 per ounce level, strong bottoming signals appeared, after which the gold price began a solid recovery.

This shows that underlying demand for gold remains whenever the price pulls back far enough.

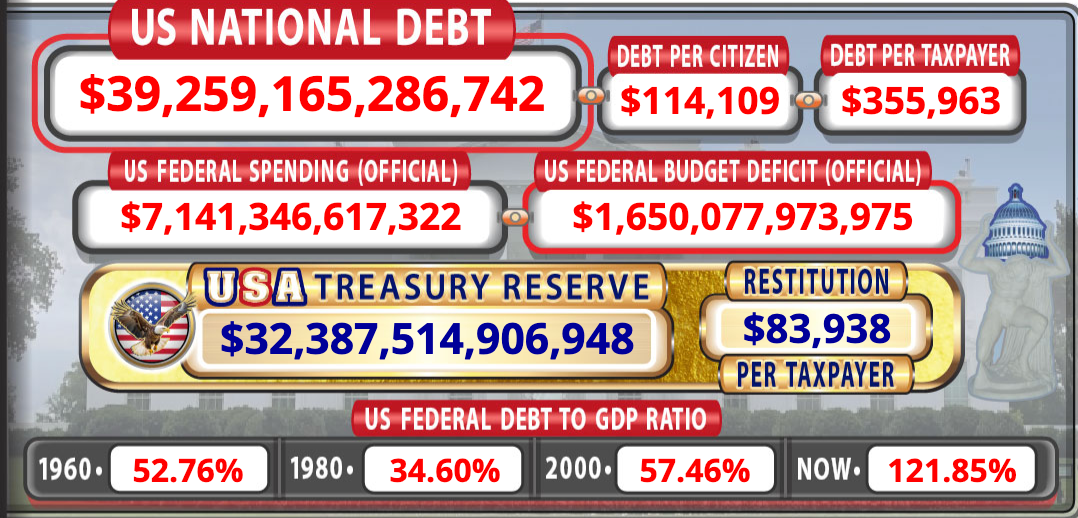

The broader fundamental picture also holds up. US national debt has now grown to approximately $39 trillion. At the same time, the US economy is still performing reasonably well, yet the government continues to run a budget deficit of around 6 percent of gross domestic product.

That is an important signal. If a government runs such deficits in a relatively strong economy, the problem only grows larger once growth cools.

Add to that the fact that higher interest rates are driving up debt servicing costs further. An ever-larger share of the budget is therefore going towards paying interest on existing debt. This creates a vicious cycle. Higher debt leads to higher interest costs, and higher interest costs widen the deficit further.

For now, that theme is not central to the market. Investors are focused primarily on AI, corporate earnings, geopolitical risks, and the direction of interest rates. But debts do not disappear simply because the market is paying less attention to them.

That is ultimately the heart of the gold story. The recent weakness is well explained by a combination of profit-taking, higher rates, a stronger dollar, AI euphoria, and capital flows towards industrial commodities. But none of those factors undermine the structural case for gold.

As long as governments structurally spend more than they take in, national debts continue to rise, and central banks ultimately find themselves trapped between fighting inflation and maintaining financial stability, gold remains a logical insurance policy in a portfolio.

That is precisely why investing in gold may be interesting at this stage. Financial assets are often best bought at moments when they are temporarily out of fashion, however uncomfortable that feels in practice.

The key prerequisite is of course that you still believe in the future story of the asset in question. For gold, that story revolves around scarcity, rising debt, structural budget deficits, and the risk that central banks are ultimately forced back towards loose monetary policy.

Gold is under pressure from AI euphoria, rising commodity demand, and higher interest rates. Why the fundamental outlook for gold remains strong nonetheless.

Thom Derks writes for GoldRepublic on gold, macro-economics and geopolitics. He studied Law in Leiden and Economics in Amsterdam. His personal fascination with scarcity and store of value through both bitcoin and gold brought him into the world of financial journalism. Through his own newsletter De Geldpers on Substack, he reaches over 5,800 subscribers with analyses on markets, geopolitics and the monetary system.